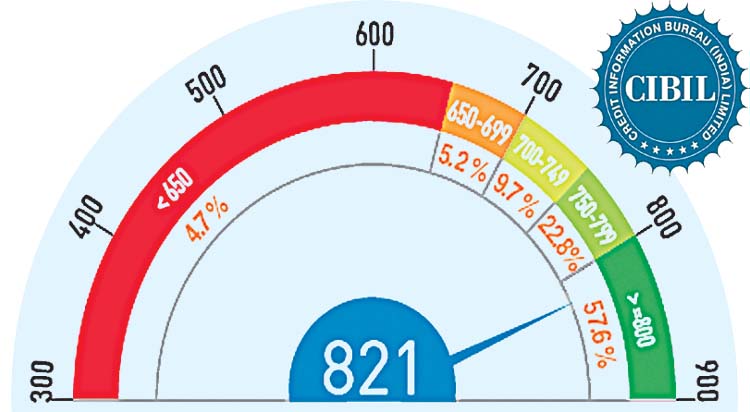

A good CIBIL score indicates higher credit worthiness through responsible past credit behaviour as reflected in the ‘Accounts’ and ‘Enquiries’ section of your CIR, ranges between 300-900. A score above 700 is generally considered good. Thus, it indicates reduced default risk for the lender. Scores above 800 are considered high and you can easily ask for a lower rate on personal loans and credit cards.

A personal loan is one of the most popular borrowing options for individuals seeking quick access to funds for a variety of personal reasons. However, the unsecured (collateral-free) nature of this loan makes it vitally important for lenders to ensure the credit worthiness of the applicant. In this regard, one of the first things that prospective lenders look at is the credit score of the loan applicant. With TransUnion CIBIL being arguably the most popular provider of credit score in India, the importance of a good CIBIL score (750 and higher) for securing a personal loan cannot be overstressed.

TransUnion CIBIL Limited is India’s first Credit Information Company, also commonly referred as a Credit Bureau. We collect and maintain records of individuals’ and commercial entities’ payments pertaining to loans and credit cards. These records are submitted to us by banks and other lenders on a monthly basis; using this information a CIBIL Score and Report for individuals is developed, which enables lenders to evaluate and approve loan applications.

A good score for secured loans. However, for unsecured credit, the bank might investigate further (like social score) or impose slightly higher rates. When you are considering a loan or checking the eligibility requirements of various lenders, you may have come across something called your CIBIL credit score. With every article you read and every experienced borrower you meet urging you to check your credit score, knowing what it is and why it is so important in the process of taking a loan is paramount. Here’s everything you need to know about CIBIL score and your CIBIL credit score.

Cibil Is India’s First Credit Information Company

Your credit score is often referred to as your CIBIL score because CIBIL stands for the name of the credit bureau that creates the score. CIBIL used to refer to the Credit Information Bureau (India) Limited. In 2000, it partnered with US-based TransUnion and the company is now called TransUnion CIBIL Ltd. CIBIL is the oldest credit information company in India, and functions based on a license granted by the RBI. It adheres to the Credit Information Act of 2005 and records the repayment of loans and credit cards by both individuals and companies. So, if you have ever availed or applied for credit, CIBIL has your information as it is updated by lenders like banks, credit card companies, and NBFCs on a monthly basis.

Cibil Creates Your Credit Report

Using this information related to your credit activities, the company creates your CIBIL report or Credit Information Report (CIR). Your repayment and borrowing history, on-going loans, credit card dues, etc., are all compiled by CIBIL and presented in your CIBIL report. It also contains your employment history and loan enquiry information. You can check your credit score and all these details by downloading this report from the CIBIL website. Doing this helps you stay informed about your credit record, and helps you report errors, if any, to CIBIL. Now, you can check CIBIL score for free with Bajaj Finserv at no extra cost. All you have to do is enter your details and access your credit score for free.

Your Cibil Credit Score Is Derived from This Credit Report

Apart from creating a credit report that details your credit history, CIBIL also gives you a credit score. Even companies have a commercial CIBIL score based on their credit history and credit report. Your CIBIL credit scorewill keep changing based on your credit report and your credit behaviour. For example, if you miss EMIs or make 5 personal loan enquiries in quick succession, your credit score will drop. On the other hand, when you pay your EMIs on time, prepay your loan, or pay the full amount due on your credit card on time, your CIBIL credit score will increase.

Your Credit Score Is Important to Lenders to as Certain Your Credit Worthiness

Just as lenders provide CIBIL with your credit-related information, they also access the same from CIBIL from time to time. As your CIBIL credit score denotes how good your credit history has been, it is used to judge your credibility when you apply for any form of credit, including instant personal loan.

A negative CIBIL score means no available credit history. If your CIBIL score is negative, then you can apply for a credit card to start your credit history. It takes 6 months of credit history to calculate a CIBIL score. A score lower than 750 is considered as a low CIBIL score. Banks generally do not sanction personal loans of people with a low CIBIL score, or even if they do, they may charge a very high rate of interest. On the other hand, untimely payment of dues and EMIs will have a negative impact on your CIBIL score.