Not all emerging markets are equal

Looking ahead, there are many reasons to remain optimistic towards emerging market equities, which we expect to benefit from a combination of long-term structural growth drivers and more recent developments, including industry consolidation and acceleration of technological/internet trends. However, selectivity remains paramount, as volatility levels remain elevated. Against this backdrop, we remain committed to our investment approach ? focused on identifying companies characterised by robust corporate governance and balance sheet structures.

Key points

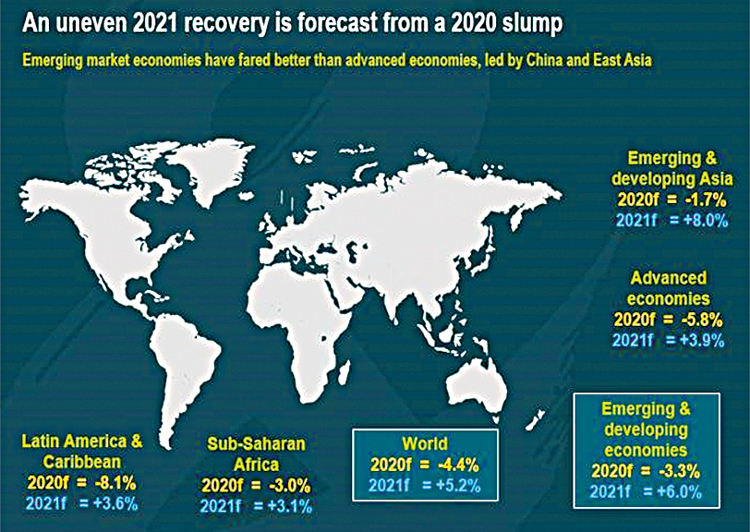

• Polarisation across the universe is likely to remain evident. While the recovery has initially been led by Northern Asia, other emerging markets (EMs) are likely to catch up.

• Interest rate regimes, inflationary pressures, direction of international trade, and industry consolidation are amongst the key trends to watch, with strong implications for various pockets of the universe.

• On balance, we remain constructive and we aim to minimise the negative impact from single events through rigorous portfolio construction and focus on intra-stock correlation.

What is your investment outlook for emerging market equities in 2021?

Polarisation across the universe is likely to remain evident. While the global recovery has initially been led by Northern Asia, other EM markets are likely to catch up as we move forward, supported by the deployment of the vaccine and rising external demand. However, because cross-country variation in fiscal policy has been large, concerns over debt sustainability in certain pockets will remain, supporting the case for selectivity. The unprecedented levels of governments’ stimulus are also likely to raise inflationary pressures. As these pressures mount, many commodities can provide a natural inflationary hedge, underpinning the case for selective exposure to the Latin America and Europe, the Middle East and Africa (EMEA) regions. Overall, we remain constructive in the face of further waves of COVID-19, with the view that these are manageable, and we focus on identifying high quality names that can navigate these more challenging waters.

What do you think could surprise the market in 2021?

As bottom-up stock-pickers, the main source of risk comes from stock selection and therefore, the catalysts are also stock-specific in nature. As ever, we aim to minimise the negative impact from single events through rigorous portfolio construction and focus on intra-stock correlation. As sentiment towards hardly hit Latin America and EMEA regions improves, supported by a pick-up in activity as well as pricing support for commodities driven by inflation, we could see a sharp re-rating, emphasised by the historically low valuations. As these markets attract flows, this could also translate into a risk as we would likely see significant downward pressure on more extended parts of the universe, such as China and broader North Asia. Growing regulation is also a risk worth flagging, as evidenced by the more recent Chinese government’s step-up in anti-trust rules in the internet space.

What themes, sectors or regions would offer opportunities or potential risks in a post COVID-19 world?

Looking at broader markets, the crisis unequivocally heightened the correlation levels across asset classes. This can have important implications for risk management in both absolute and relative terms, particularly in instances of large momentum moves. More specifically to EMs, we expect heightened levels of industry consolidation across the board, with larger brands set to benefit from this backdrop; this is particularly evident in the consumer and technology sectors. Importantly, whilst the pandemic has served as a further catalyst for digitalisation, with internet/tech-related names likely to benefit from this, structural growth drivers such as urbanisation, financialisation and lifestyle changes persist and will continue, indicating opportunities also across a range of more traditional domestic businesses. We also continue to keep an eye on inflationary and interest rate considerations, with their implications for resources and financials names respectively.

Within your portfolio, what areas have highest convictions and what areas are you avoiding?

The rising purchasing power of emerging market consumers indicates opportunities in many consumer-related businesses across a range of segments. We have exposure to structurally sound companies operating across an array of sub-sectors, going beyond purely internet-related names to include autos, sportswear and cookware, amongst others. Our focus on domestic names is particularly important in the context of decreasing multilateralism, as we seek to invest in companies that can perform well despite lower levels of international trade. Leading hardware manufacturers also sit in the portfolio, given the favorable backdrop for technological advancement.

Given the inflationary backdrop and economic recovery, we are selectively exposed to commodities, including copper, steel and Platinum Group Metals (PGMs). Elsewhere, we remain cautious on financials, given the prevailing low interest rate environment and its impact on banks’ ability to sustain attractive levels of profitability. Given our view for a weaker pricing environment for oil for longer, we are not finding opportunities in the energy space at present.

How do you expect sustainability factors to influence returns and how is this reflected in your portfolios?

We believe that ESG considerations will continue representing key drivers of returns. It will thus be key to maintain a focus on identifying businesses with best-in-class practices, reflecting in clear ESG policies articulated by experienced management teams, who are able to deliver (and pass on) attractive returns to shareholders. Importantly, the recent crisis has also highlighted the importance of investing in high quality names, characterised by sound balance sheet structures that enable them to weather more challenging environments and come out stronger from the volatility than peers. Our focus on governance and capital structures will thus remain paramount, in driving alpha for our investors and avoiding permanent loss of capital.